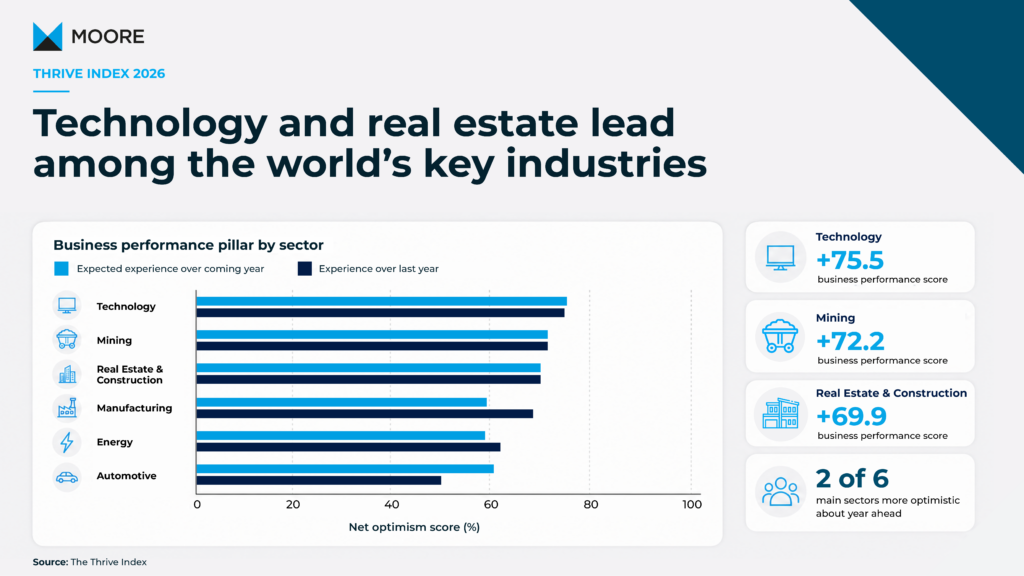

Technology and real estate businesses bucked the trend among the main sectors of the global economy and reported above-average levels of optimism in the latest Moore Thrive Index.

In technology, the driving force is investment in AI and new digital tools. Over the coming year, 75% of businesses expect to increase spending, with more than one-third expecting to increase levels by more than 10%.

Property suffered more than most over the past few years, with elevated inflation pushing up building costs and higher interest rates making funding projects more expensive.

Confidence is returning now, resulting in real estate recording a total score of +38.2 in our Thrive Index, while the total score for technology was even stronger at +43.3. These scores compared with a global average of +35.1.

Moore’s Thrive Index is a unique research project that combines the actual experience of those running mid-market companies over the past year with their confidence about the future. It captures the balance of positive to negative scores on five key pillars across 17 economies: business sentiment, revenue, costs, the labour market and investment.

It has been a mixed year for the main pillars of the global economy with a perfect storm of factors including geopolitical tension, economic uncertainty and rising costs having a negative impact.

Four out of six key sectors that collectively account for around 60% of global GDP, reported below-average levels of optimism in the Thrive Index compared to the global average. These include automotive, energy, manufacturing and mining.

However, there is optimism about the year ahead as they see ways through the challenges that have curtailed growth.

Jeff Blackbeard, Chief Growth Officer at Moore Global said:

“The story of the past year has been one of resilience under pressure. Mid-market businesses remain positive on balance but are approaching the year ahead with more caution.

“Businesses have adapted remarkably well to a backdrop of geopolitical uncertainty, inflationary pressures and shifting market conditions.

“At the same time, leaders are telling us that growth is becoming harder to predict. They remain optimistic, but they are becoming more selective about investment, recruitment and expansion decisions.”

Automotive

Sector Index Score +34.1 … -1.0 v Global Average

Despite increased tariffs and broader economic headwinds, 2025 proved to be a resilient year for the industry.

The International Organisation of Motor Vehicle Manufacturers (OICA) said global vehicle production grew 3.9% last year and global sales increased by 4.7%.

However, there was clear evidence of a competitive shift in the industry, with Asian manufacturers – specifically Chinese – becoming a dominant force. Their growth has impacted European car makers and suppliers.

Almost 60% of businesses expect their revenues to increase over the coming year compared to the last 12 months. That compares with 23% that anticipate their revenues will fall.

Hiring activity proved more resilient in the automotive industry compared to other sectors, with almost two-thirds of companies reporting increased headcount in the past year.

Looking ahead, a lower share of businesses expect to increase their workforce over the coming year compared to last year but the overall score remains positive on balance.

Real Estate & Construction

Sector Index Score +38.2 … +3.1 v Global Average

The sector broadly outperformed the overall Thrive Index, with the strongest scores recorded over the past year in general business performance, investment activity and revenue.

This resilience is consistent with moderating inflation and a more supportive interest rate environment experienced over the past year, prior to the energy price shock at the start of 2026.

However, the industry reported higher-than-average cost pressures. Two-thirds of businesses reported cost increases over the past year compared to the previous 12 months.

Looking ahead, those pressures are expected to persist, with 69% of businesses expecting increases, compared to 14% that foresee a reduction.

The main drivers of expected expenses increases are interest rates and financing, followed by raw materials and energy.

Meanwhile, renewed inflationary pressures have led to tighter financial conditions for the year. A higher interest rate environment could weigh heavily on companies, given their reliance on external finance and the sensitivity of property demand to borrowing costs.

Overall, firms remain upbeat on balance about future investment intentions, with 62% of planning to increase levels compared to last year.

Energy

Sector Index Score +30.8 … -4.3 v Global Average

The result for the energy sector suggests that recent conditions have been more subdued than in other industries. Expectations for the coming period remain comparatively cautious but positive overall.

The sector’s labour market performance was relatively weak, with an overall Index score of 30.6 on this measure, compared to the average score of +41.6. Over the past year, only half of businesses increased headcount relative to the previous 12 months. The lower hiring trend looks set to continue in 2026.

On costs, the picture is more mixed, with data suggesting less severe upward pressure overall. Looking back over the past year cost conditions are broadly in line with the Thrive Index sample, while forward-looking cost expectations are notably more benign.

However, sustained volatility in global energy markets with continued risk of supply interruptions, suggest these predictions on costs remain vulnerable to geopolitical developments.

Manufacturing

Sector Index Score +33.7 … -1.4 v Global Average

Tariff escalation, continued cost pressures and key labour shortages in some countries all posed significant risks to the manufacturing sector.

Business performance held up relatively well over the past year, supported by improvements in operational efficiency and workforce productivity.

The survey pointed to strong investment activity over the past year, with almost 73% of businesses increasing their spending levels over the past year relative to the previous 12 months. One-fifth of companies boosted levels by more than 10%.

The areas that saw the largest shift in investment were technology and digital tools and developing new products or services.

Sentiment is slightly weaker among manufacturing businesses for the coming year. Ongoing trade and geopolitical uncertainty continue to create risks around global supply chains and export demand. They also contributed to upside inflation risks that could increase raw material and input costs.

Additionally, businesses may be anticipating softer demand conditions amid expectations of more subdued global growth.

Mining

Sector Index Score +32.5 … -2.6 v Global Average

Sentiment regarding overall business conditions remained relatively resilient, reflecting favourable conditions in commodity markets that are pivotal to profitability.

The World Bank predicts the metals and minerals price index will rise by 17% year-on-year in 2026, supported by strong underlying demand and supply constraints.

In particular, the growing clamour for renewable energy and expanding data centre infrastructure has continued to support prices for critical minerals, helping to sustain profitability across the sector.

Investment intentions for the coming year are also holding up well. A net balance of firms expecting to increase investment resulted in a score 5.4 points above the global average on this measure of the Index.

Seven-in-ten businesses reported plans to raise investment over the next year, with sustainability and environmental initiatives cited as the main areas of focus.

However, positive demand dynamics are being counteracted by persistent cost pressures, with energy and fuel costs the most significant sources of cost pressure.

This is consistent with wider industry trends, including higher energy prices, rising labour costs and increasing ESG requirements associated with decarbonisation.

Technology

Sector Index Score +43.3 … +8.2 v Global Average

The technology sector outperformed the global average, demonstrating a strongly confident outlook despite broader economic headwinds and downside risks to global growth.

The strongest score of the forward-looking metrics was on business performance, with 83% of companies expecting better performance over the coming year. Only 7.5% expect it to worsen.

Rising cost pressure continues to present a challenge. Interest rates and labour were the two main cost worries over the past year. They remain a concern going forward, followed by raw materials.

Stronger-than-average expectations for future business and revenue performance in the industry underpin comparatively stronger investment intentions. Maintaining strong investment will be critical to supporting technological development, AI integration and long-term competitiveness.

Over the coming year, 75% of businesses expect to increase investment levels, with more than one-third expecting to increase levels by more than 10%.