War, energy supplies and political tensions are having a significant impact on the mid-market businesses that form the backbone of the world’s supply chain, according to Moore Global’s latest Thrive Index.

Overall business performance has been remarkably resilient over the past 12 months but firms expect lower revenues over the next year, which they say will impact employment and investment.

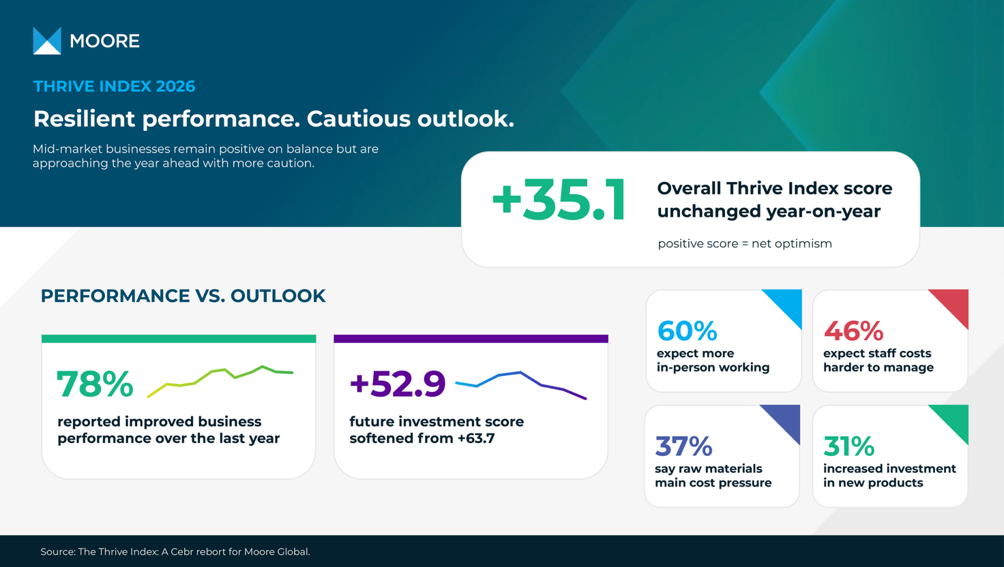

The Thrive Index is a unique research project that combines the actual experience of leaders of mid-market companies over the past year with their confidence about the future on key measures that are crucial to success.

It represents the balance of positive to negative scores on five key pillars: general business sentiment, revenue, costs, the labour market and investment.

The latest Index score is unchanged from +35.1 recorded in 2025 – but the data reveals far greater uncertainty about the impact of geopolitical factors, subdued demand and input costs over the rest of the year.

Business performance remained resilient over the last 12 months, with three-quarters of companies reporting improvements. Looking ahead, sentiment remains positive overall but there is much more caution about growth prospects.

Eight countries – South Africa, Saudi Arabia, UAE, India, US, China, Australia and Brazil – all recorded higher overall Thrive Index scores than the average. Meanwhile European countries, along with Japan and Canada, recorded below-average scores.

The split starkly demonstrates the shifting balance of power in the world economy.

It is no coincidence that those countries powering ahead are either benefiting from the boom in critical mineral prices or the widespread adoption of AI and other digital technologies to carry out tasks once performed by human workers.

On almost every measure in the Thrive Index, IT and sectors rapidly adopting new technology are more optimistic about the future.

General Business Sentiment

Thrive Index score +68.8 v +66.3 last year (+0.5)

Business remained resilient last year, with 77.8% of businesses reporting improvements in their business performance. Looking ahead, sentiment remains positive overall but more cautious.

This reflects a deterioration in the global growth outlook for the coming year, as geopolitical developments have heightened uncertainty and reinforced expectations of persistently higher inflation, energy costs and interest rates.

Banking recorded the highest score on sentiment and with a score of +74.5 shows great confidence in the next 12 months, with anticipated improvements in performance expected to be supported by the adoption of technology and improved workforce productivity.

Automotive and retail sectors recorded amongst the lowest scores over the past year, reflecting their greater exposure to supply chain pressures and ongoing global trade uncertainty. However, both sectors are far more optimistic about the coming year.

Across countries, the strongest forward-looking business performance score was +80.0,

jointly recorded by the UAE and South Africa.

Despite the heightened geopolitical risk facing the UAE, the business outlook remains strong, supported by the adoption of technology and the expansion into new customer and geographical markets. South Africa is benefiting from structural reforms that have improved access to international capital.

Around one-third of businesses recording improved performance over the past year cited adoption of technology or digital transformation as one of the three main factors. This was particularly marked in Brazil and South Africa.

Improved operational efficiency was the second most important factor in producing a positive outlook: the UK was the standout country here, with almost half of businesses reporting efficiency gains over the past year.

Three out of ten companies reporting worse performance over the last year blamed unfavourable macroeconomic trends that resulted in subdued consumption, restrictive monetary policy, as well as heightened trade and tariff uncertainty.

A similar number expect those to drive further deterioration in performance over the coming year.

Revenue

Thrive Index score +58.4 v +59.1 last year (-0.7)

Despite a big jump in reported revenue over 2025, there are doubts about what the future holds. A deterioration in future revenue expectations has led to a slight decline in the score for this pillar compared to last year.

Of the 17 countries included in the analysis, only China and the UK were more optimistic looking forward, with around three-quarters of firms in both countries anticipating an improvement in sales. The experience of Saudi Arabia and UAE firms was well above average last year but both expected weaker growth ahead.

Performance and levels of expectation vary significantly when company size is taken into account.

Those with up to 500 employees recorded much lower scores than firms employing more than 1,000 people. This reflects their greater exposure to domestic demand conditions, a narrower customer base and more limited financial buffers, leaving them more sensitive to uncertainty and cost pressures than larger businesses.

Business Costs

Thrive Index score -49.5 current v -49.8 last year (+0.3)

Conflict in the Middle East has already translated into an acceleration in inflation, driven by supply disruptions and energy price shocks. These pressures are expected to persist in the near-term.

It leaves businesses facing rising costs amid renewed inflation risks, so it is no surprise that negative scores were recorded unanimously across this pillar of the Index.

The most pessimistic score for the year ahead, -61.0, came from the UK, which is already struggling with stubborn inflation and has among the highest energy costs in Europe.

The world’s big industrial producers all scored -40.0 to -50.0 for the year ahead, although a number of European countries were considerably more optimistic. Italy and the Czech Republic both scored well above -20.0.

Across sectors, telecommunications experienced the toughest 12 months, scoring -61.5, underpinned by high logistics and labour costs.

On the forward-looking measure, the worst score was recorded by technology, at -55.4, with those expecting cost changes to be driven by interest rates, financing and raw material costs. The sector’s high dependence on external financing and capital-intensive investment makes it particularly vulnerable to elevated interest rates.

Labour costs remain a burden to businesses and concerns about energy costs are growing.

Over the coming year, 37.0% of businesses surveyed predicted raw material costs would be the main driver of cost increases.

Meanwhile, concerns over energy costs appear to have increased for the coming year. Persistently high prices could place further upward pressure on energy-intensive sectors like manufacturing and transport, while also contributing to broader inflationary pressures across supply chains.

Labour Market

Thrive Index score +41.6 v +42.3 last year (-0.7)

Over the past year, higher labour and input costs have contributed to a gradual slowdown in hiring and an easing in labour market conditions. While headcount growth remained positive on balance, signs of further slowdown are expected over the coming 12 months.

Most European firms recorded neutral or negative scores, meaning they expect to maintain or reduce headcount over the next year. Even the highest scores of around +60.0 in the expanding economies of South Africa and India, have drifted back to nearer +50.0 for the year ahead.

Almost 46% of those surveyed said it will become more difficult to meet staff costs over the coming year, while a similar number (45.4%) said it will be more of a struggle to retain existing staff.

Softer hiring expectations and concerns around recruitment are exacerbated by general cost pressures bearing down on companies.

More than 50% of business leaders in hospitality, marketing and media and financial services expect hiring difficulties. Hiring issues in hospitality reflect labour supply constraints and high staff turnover while the other sectors highlighted are undergoing huge structural change with rising demand for specialist digital, analytical, and AI-related skills. Working from home has been credited with helping to attract and retain people since Covid but the new Thrive Index reveals increasing employer frustration with the concept. Almost 60% of respondents said they were likely to restructure towards more in-person working over the coming year

Investment Activity

Thrive Index score +58.3 v +57.6 last year (+0.7)

Over the past year, 70% of businesses reported growth in investment levels. However, this momentum is likely to be moderated by a subdued global growth outlook, softer demand, more restrictive monetary policy and heightened uncertainty.

The vast majority of companies in our global survey reported higher investment levels last year as the high inflation and interest rates of 2024 began to ease. However, there is a nagging worry that inflation risks inherent in heightened geopolitical tensions will flow through to more restrictive monetary policy and higher borrowing costs.

The sector that seemed most insulated from these concerns was technology, which backed up last year’s strong performance with an index score of +66.4, underpinned by tech companies’ potential for scalable innovation and productivity gains.

Across all industries, some 31.0%, expect to change their investment levels in developing new products or services over the coming year.

With the next wave of digital transformation and adoption of AI underway, firms are prioritising tech investments to enhance productivity and operational efficiency.

Brazil stands out, with almost half of businesses (48.6%) citing technology and digital tools as the most significant drivers of change in investment over the past year. A similar proportion are predicting the same for the coming year, supported by government-led initiatives which aim to position Brazil as a global leader in AI.

Another major investment area over the past year was strengthening cybersecurity and data protection, cited by 28.9% of businesses. This reflects the increased cyber and data security risks that come with greater adoption of AI and other digital technologies.