IAS 36 Impairment of Assets

Tax Guide: IAS 36 Impairment of Assets

SCOPE

IAS 36 applies to all assets except for the following:

- Inventories (IAS 2)

- Contract assets (IFRS 15)

- Deferred tax assets (IAS 12)

- Assets arising from employee benefits (IAS 19)

- Financial assets (IFRS 9)

- Investment properties measured at fair value (IAS 40)

- Biological assets measured at fair value less costs to sell (IAS 41)

- Insurance contracts in scope of IFRS 17

- Non-current assets held for sale (IFRS 5)

IAS 36 does apply to investments in subsidiaries, associates and joint ventures.

WHEN TO PERFORM AN IMPAIRMENT TEST

At the end of each reporting period entities should assess both internal and external sources of indicators to determine whether an asset may be impaired. Indicators may include:

- Obvious decline in market value of an asset

- Adverse technological, market, economic or legal conditions

- Increasing market interest rates

- Net assets is greater than market capitalisation

- Obsolescence or physical damage

- Idle assets

- Restructuring plans

- Performance of asset is declining

If indicators exist a detailed impairment test must be performed.

Goodwill and intangible assets with indefinite lives; and intangible assets not yet available for use shall perform a detailed impairment test annually.

DETAILED IMPAIRMENT TEST

A detailed impairment test is calculated as follows

The recoverable amount is the higher of

- value in use; and

- fair value less costs of disposal.

If one of these is greater than the carrying amount of the asset, there is no need to determine the second, as no impairment will need to be recognised.

Value in use

The Value in use (VIU) is the present value of cash flows expected to be generated from the use of the asset. A VIU:

- Reflects entity specific intentions and use

- Reflect cash flows from its current condition and use and not expected uncommitted restructures or cost savings, on future enhancements

- Reflect cash flows from continuing use and ultimate disposal

- No more than 5 years explicit forecasting unless a longer period can be justified

- Pre-tax cash flows and discount rate

- Risks should be reflected either in cash flows or discount rate but not in both

- Financing cash flows and income tax receipts or payments should be excluded

Fair value less costs of disposal

Fair Value less costs of Disposal (FVLCD) reflects the fair value calculated in accordance with IFRS 13 Fair value measurement less any costs attributable to the disposal of the asset. FVLCD therefore reflects market expectations of the price at which the asset will be sold.

CASH GENERATING UNITS AND GOODWILL

If it is not possible to determine the recoverable amount of an individual asset, the asset should be grouped into Cash Generating Units (CGUs).

CGUs are the smallest group of identifiable assets that generates largely independent cash inflows.

At the time of a business combination, goodwill shall be allocated to a CGU or the group of CGUs that are expected to benefit from the combination, and be assessed annually for impairment as part of that CGU.

In testing a CGU for impairment, entities shall identify all the corporate assets that relate to the CGU under review.

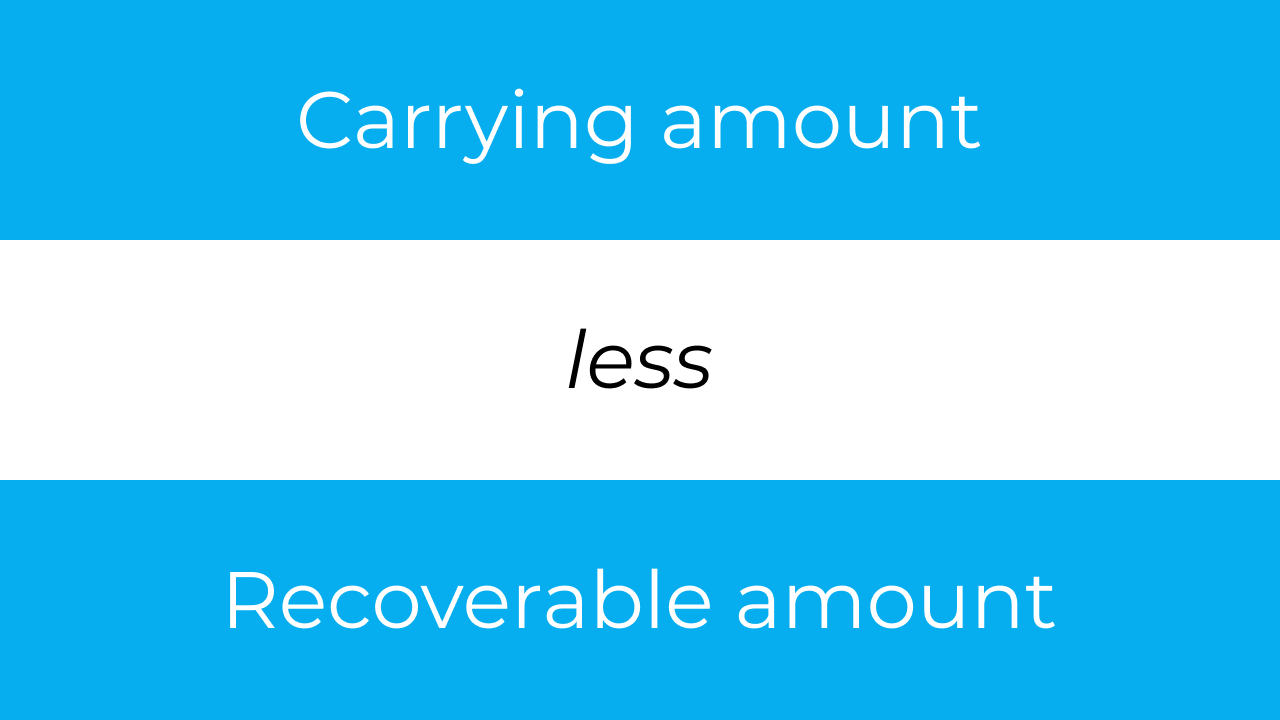

RECOGNISING IMPAIRMENT

Impairments are recognised when the recoverable amount is less than the carrying amount of the asset of the CGU.

Impairment losses are recognised immediately in profit or loss unless the asset is carried at a revalued amount with valuations recognised in a revaluation reserve (e.g. property, plant and equipment at fair value in accordance with IAS 16) in which case the impairment loss is first recognised against the revaluation reserve until it is reversed to Nil then the remainder is recognised in profit or loss.

If an impairment loss is required to be recognised for a CGU it is allocated:

- First to any goodwill attributable to the CGU

- To all other assets in the scope of this standard in the CGU on a pro-rata basis

In allocating an impairment loss, carrying amount of an asset should not be reduced below the highest of:

- Its fair value less costs of disposal

- Its VIU

- Zero

The amount of impairment loss that would otherwise have been allocated to the asset shall be allocated pro rata to the other assets of the CGU.

REVERSING IMPAIRMENT

Impairments may be reversed in subsequent periods for all assets other than goodwill. At the end of each reporting period entities shall assess both internal and external sources of indicators to determine whether an impairment loss recognised in prior periods for an asset other than goodwill may no longer exist or may have decreased. Impairments are reversed if there is a change in the estimates used to determine the recoverable amount since the last impairment loss was recognised.

Impairments are reversed through the income statement, unless the asset is revalued through a revaluation reserve.

A reversal of an impairment shall not increase the value of the asset beyond what the carrying amount would have been if the impairment had never been recognised, after taking into account the impacts of depreciation and amortisation.

DISCLOSURES

Detailed disclosures are required where detailed impairment assessments are undertaken to explain the assumptions and inputs used in the valuation process. Where no impairment loss is recognised,

but a reasonable possible change in assumptions would lead to an impairment loss, that sensitivity analysis should be provided. Additional information is required around the use of CGUs and the allocation of goodwill as well.

CONTACTS

| BOAZ DAHARI Moore Israel [email protected] | KRISTEN HAINES Moore Australia [email protected] | TAN KEI HUI Moore Malaysia [email protected] |

| CHRISOF STEUBE Moore Singapore [email protected] | NEES DE VOS Moore DRV [email protected] | TESSA PARK Moore Kingston Smith [email protected] |

| EMILY KY CHAN Moore CPA Limited [email protected] | PAUL CALLAGHAN Moore Oman [email protected] | THEODOSIOS DELYANNIS Moore Greece [email protected] |

| IRINA HUGHES Johnston Carmichael [email protected] | SAHEEL ABDULHAMID Moore JVB LLP [email protected] |

MOORE IFRS in Brief is prepared by Moore Global Network Limited (“Moore Global”) and is intended for general guidance only. The use of this document is no substitute for reading the requirements in the IFRS® Accounting Standards issued by the International Accounting Standards Board (IASB). This document reflects requirements applicable as at the date of publication, any amendments applicable after the date of issuance, to the IFRS® Accounting Standards have not been reflected. Professional advice should be taken before applying the content of this publication to your particular circumstances. While Moore Global endeavors to ensure that the information in this publication is correct, no responsibility for loss to any person acting or refraining from action as a result of using any such information can be accepted Moore Global.